量化宽松加速退场 美联储的资产持仓总量缩水850亿美元

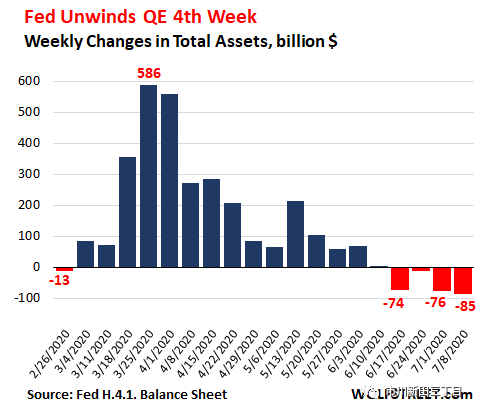

量化宽松加速退场:美联储的资产持仓总量缩水850亿美元,过去四周共减持2480亿美元的资产

来源:市川新田三丁目

译者 王为

文中黑字部分为原文,蓝字部分为译文,红字部分为译者注释或补充说明

QE Unwind Speeds Up: Fed’s Assets Drop $85 Billion. Four-Week Total -$248 Billion. Big Chunk in a Short Time

by Wolf Richter

Repos & dollar liquidity swaps on their way out. SPVs declined. Hardly bought any corporate bonds & ETFs. MBS flat. Treasuries ticked up.

OK, this balance-sheet shrinkage, now in its fourth week, is going faster than I’d expected. Total assets on the Fed’s balance sheet for the week ended July 8, released this afternoon, dropped by -$85 billion, the fourth week in a row of declines. This brought the four-week total drop to -$248 billion:

美联储资产负债的总量已连续第四个星期减少,速度比我原先预计的要快。美联储在7月9日宣布,截止到7月8日为止其资产负债表上的总资产较前一周缩水了850亿美元,连续第四周下行,过去四个星期资产减持总量达到2480亿美元。

Back on April 9, when markets were just emerging from chaos after the Fed had thrown $1.5 trillion at them in the span of four weeks, Fed Chair Jerome Powell said in a webinar at Brookings that “when private markets are once again able to perform their vital functions of channeling credit and supporting economic growth, we will put these emergency tools away.”

在此之前的4月9日,市场因美联储在四个星期的时间里豪掷1.5万亿美元纾困资金后刚刚从一片混乱中获得一丝喘息,当时美联储主席鲍威尔在布鲁金斯学会举办的一场研讨会上表示,“一旦以私营企业为主导的金融市场能够再次发挥出顺畅融资的功能并有效支撑经济的运行,我们就将撤回这些紧急纾困举措。”

This matched what he and other Fed officials had said in the year or so before the Crisis, that at the “next crisis,” they would throw all the Fed’s might at the problem up front, and then they’d back off, rather than let QE drag on for years. And they did.

这一最新的表态与他以及其他联储官员在本次危机爆发之前一年左右的时间里的说法相吻合,当时的说法是,如果下一场危机到来联储会使出浑身解数“先下手为强”,但在危机得到遏制后会及时脱身而不是让量化宽松的做法迁延数年,如今他们说到做到了。

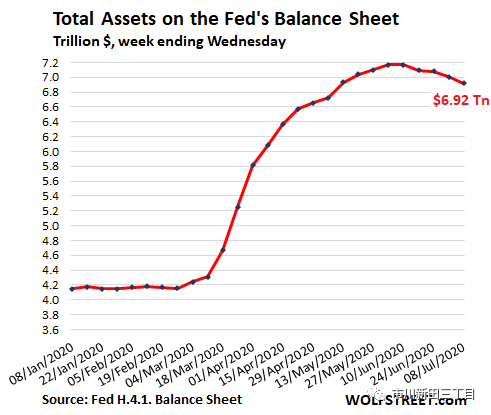

By peak-QE in early June, the Fed had increased its assets by $2.86 trillion. It has since then whittled this increase down by $248 billion. Note the systematic front-loading then tapering the asset purchases and letting assets top out at $7.16 trillion, and then letting them decline, now down to $6.92 trillion:

在6月初本轮量化宽松的巅峰时刻,美联储增持了2.86万亿美元的资产,从那之后开始逐步减少,最新值下降了2480亿美元。要注意这是有计划有步骤地操作,先把资产规模拱到最多时的7.16万亿美元,然后再开始削减资产买入的力度任由资产持仓总量下行,如今的资产规模为6.92万亿美元。

Assets by category.

各类资产的持仓量分别是多少?

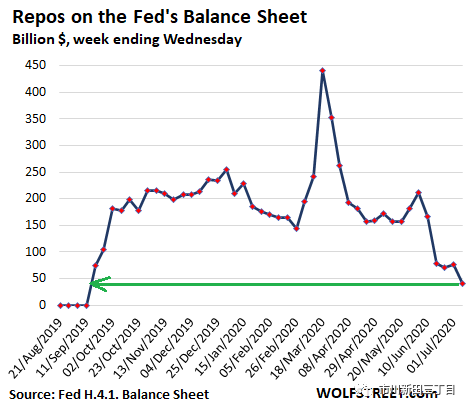

Repo balances dropped by $34 billion, to just $41 billion, the lowest since the Fed starting ramping up repos. Repurchase agreements are on the way out. There were zero overnight repos on the balance sheet, and only some older term repos that hadn’t unwound yet.

美联储回购科目的余额一周之内下跌了340亿美元,只剩下410亿美元,为去年9月份开始大举通过逆回购向市场供应流动性以来的最低值。回购交易在陆陆续续地到期,隔夜回购的余额为零,只有一些原先叙做的固定期限回购交易尚未到期。

The Fed made repos less attractive over time. On June 16, it raised the bid rate, and for market participants there are now better deals available in the repo market. The Fed is still offering theoretically huge amounts of repurchase agreements every day, but there are no longer any takers:

美联储有意识地引导回购交易逐渐变得不那么具有吸引力。联储在6月16日抬高了回购利率的报价,对于市场参与者来说如今在联储之外可以找到更好的回购交易对手。现在联储每天仍在回购市场对外询价可以提供看上去上金额似乎很大的回购资金,但问津者寥寥。

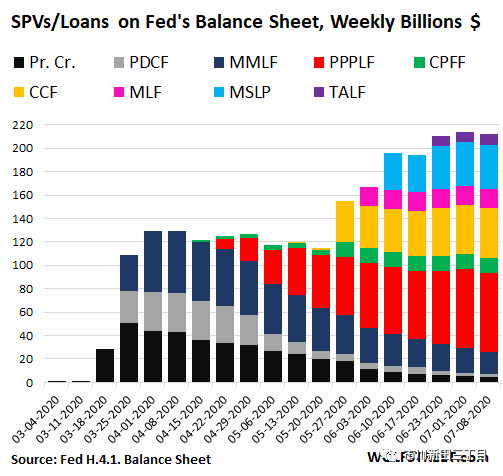

SPVs & Loans declined by $2 billion, flat for three weeks.

通过特殊目的实体和各类专项贷款计划提供的融资余额减少了20亿美元,连续三周保持平稳

The Fed’s gaggle of Special Purpose Vehicles (SPVs) have been one of the most media-hyped “tools” of the Fed, and yet, they have remained small, in terms of Fed-sized quantities. The Fed claims that these SPVs are authorized under Section 13 paragraph 3 of the Federal Reserve Act, as amended by the Dodd-Frank Act.

联储推出来的那一堆特殊目的实体是被媒体炒作最凶的政策性金融工具,但是对于一出手动不动就是天文般数字的联储来讲,其规模仍然较小。联储的说法是,出台这些特殊目的实体是根据修正后的多德-弗兰克金融改革法案中联储章节的第十三章第三段。

The way these SPVs work: The Fed creates an LLC. The Treasury Department puts in equity capital – taxpayer money as loss protection for the Fed. The Fed then lends to the LLC at a leverage ratio of 10 to 1. The LLC buys securities or lends, secured by collateral. The alphabet-soup list has been growing over the weeks:

这些特殊目的实体是这么运作的:美联储出面成立一家有限合伙企业,美国财政部出钱-也就是纳税人的钱作为资本金,来吸纳美联储投资可能的亏损。美联储再按照1:10的杠杆配资,然后这家有限合伙企业就开始买入证券或叙做有担保的资金融出。没过几个星期这些用奇奇怪怪的字母所代表的特殊目的实体的名单就越拉越长了:

-

Primary Credit (abbreviated “Pr. Cr.” on the chart below); loans made directly to lenders.

-

一级市场融资是把钱直接借给企业借款人;

-

PDCF: Primary Dealer Credit Facility

-

PDCF就是给一级交易商提供的融资便利

-

MMLF: Money Market Mutual Fund Liquidity Facility

-

MMLF就是给货币市场共同基金提供的融资便利

-

PPPLF: Paycheck Protection Program Liquidity Facility

-

PPPLF就是借钱给雇主向员工发工资的融资便利

-

CPFF: Commercial Paper Funding Facility

-

CPFF就是商业承兑汇票融资便利

-

CCF: Corporate Credit Facilities: includes the SMCCF (Secondary Market Corporate Credit Credit) and PMCCF (Primary Market Corporate Credit Facility).

-

CCF就是面向企业提供的融资便利,具体分为两种:一个是SMCCF,即二级市场企业融资便利;还有就是PMCCF,即一级市场企业融资便利;

-

MSLP: Main Street Lending Program

-

MSLP是面向中小企业的贷款计划

-

MLF: Municipal Liquidity Facility

-

MLF是给市政当局的融资便利

-

TALF: Term Asset-Backed Securities Loan Facility

-

TALF是固定期限资产质押证券融资便利

The total combined balance at these entities declined by $2 billion from the prior week and has now been roughly flat for three weeks. The original three entities (dark blue, gray, and black) are being unwound. And new ones have been added.

这些林林总总的特殊目的实体融资计划的余额加在一起与前一周相比缩水了20亿美元,已连续第三周几乎纹丝不动了。最下面的三个融资计划(见下图中的深蓝色、灰色和黑色标识部分)即将到期,新的融资计划取而代之。

The largest SPV is the PPPLF (red), at $68 billion, down a smidgen from the prior week. It buys forgivable PPP loans from banks. These loans are now starting to unwind as they’re being forgiven (taxpayers pays) or paid back by the borrower.

规模最大的特殊目的实体融资计划是途中红褐色代表的借钱给雇主向员工发工资的融资便利,余额为680亿美元,与前一周相比略有下降。该融资计划从商业银行手中买入具有违约责任豁免条款的用于雇主给员工发薪酬的商业性贷款,这些贷款正在到期,要么已经违约了(如果违约,买单的是纳税人的钱),要么就是借款企业主动偿还了贷款。

The second largest, the CCF (yellow), edged up $700 million from the prior week to $42.6 billion. This entity buys corporate bonds, bond ETFs, and corporate loans. This was the most ballyhooed of all SPVs, and it has essentially remained flat for four weeks.

第二大融资计划是图中黄线代表的面向企业提供的融资便利,最新规模为426亿美元,环比上周增加7亿美元。该融资计划买入的是公司债、投资信用债的交易所交易基金以及面向公司发放的贷款,是所有这些特殊目的实体中最扯淡的,其规模在最近四周里基本上没啥变化。

Third largest, the MSLP (baby-blue) has remained flat for the third week in a row, at 37.5 billion. It buys loans from banks that they extended to small and medium-size businesses.

第三大融资计划是图中淡蓝色线代表的面向中小企业的贷款计划,最新规模为375亿美元,该融资计划是从商业银行手中买入面向中小公司发放的贷款,其规模已连续三周保持平稳。

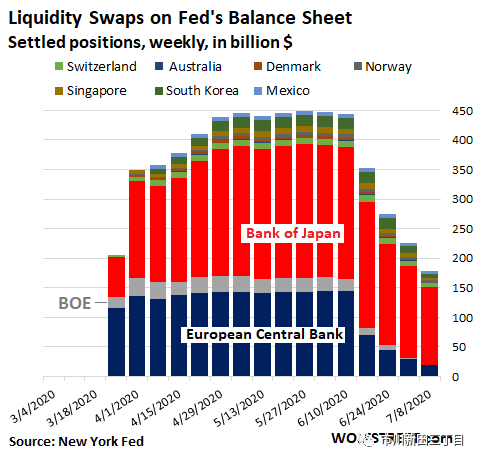

Central-bank liquidity-swaps dropped by $46 billion.

通过央行美元互换计划提供的流动性总量减少了460亿美元

The Fed’s “dollar liquidity swap lines” were designed to provide other central banks with dollars. The Fed lends newly created dollars to another central bank and takes their newly created domestic currency as collateral. The swap lines drop when swaps mature and the Fed gets its dollars back.

美联储设立的“美元流动性互换额度”旨在为其他国家央行提供美元流动性。美联储将新发行的美元提供给外国央行,外国央行反过来以新发行的本国货币为担保。在互换交易到期的时候该互换额度项下的交易余额会出现减少,美联储会在交易到期的时候回收美元头寸。

Total swaps fell by $46 billion to $179 billion, lowest since March 18. This indicates that the dollar panic overseas has dissipated. The lion’s share of the Fed’s swaps remains with the Bank of Japan – $132 billion, or 74% of the total. The Bank of England (BOE) and the Reserve Bank of Australia have essentially unwound their swaps with the Fed:

美元互换的未到期余额环比上周下跌了460亿美元至1790亿美元,为3月18日以来最低,说明海外的美元头寸紧张局面已得到缓解。大部分尚未到期的美元互换交易是与日本银行叙做的,金额为1320亿美元,相当于总交易量的74%,英格兰银行和澳大利亚储备银行与美联储之间的美元互换交易基本上到期完毕。

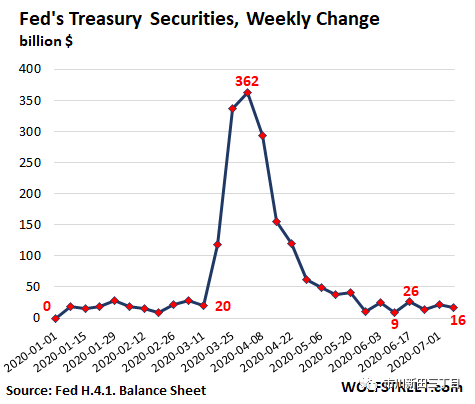

Treasury securities rose by $16 billion.

联储的美国国债持仓量增加了160亿美元

The increases in the balance of Treasury securities have been range-bound over the past seven weeks between $9 billion and $26 billion a week. This is where the Fed did a lot of heavy lifting up front:

在过去7周里,美联储每周新增持的美国国债大致位于90亿美元至260亿美元之间,通过下图可以看到美联储在危机爆发时“先发制人”地大举增持美国国债。

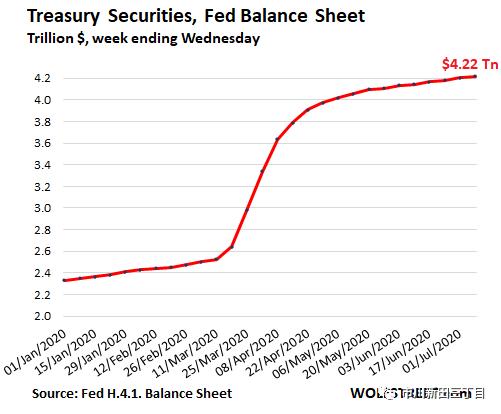

Treasury securities, now at $4.22 trillion, are by far the Fed’s single largest asset category. In its huge Treasuries portfolio, securities mature every month. The increase in the balance sheet is the net of new purchases minus redemptions. Since early March, the Fed has added $1.7 trillion in Treasury securities:

当前美联储的美国国债持仓量达到4.22万亿美元,为美联储手中最大的单一资产持仓类型。由于国债持仓量巨大,每个月都有国债陆续到期,美联储资产负债余额的增量来自于新买进的资产减去到期的资产。自三月初以来,美联储的美国国债持仓量增加了1.7万亿美元。

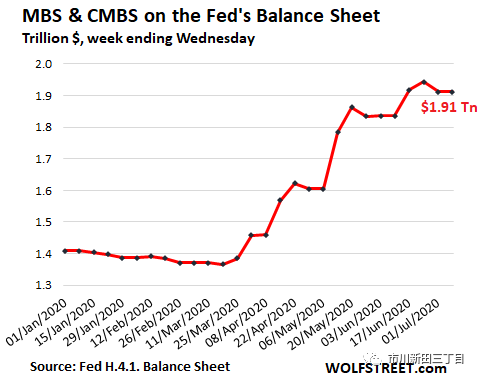

MBS remained flat.

按揭质押债券的持仓量变动不大

Mortgage-backed securities have two characteristics that cause erratic movements on the Fed’s balance sheet:

按揭质押债券的两个特点会导致美联储的资产负债总量发生难以捉摸的变化。

Pass-through principal payments. Holders of MBS receive pass-through principal payments as the underlying mortgages are paid down or are paid off. Mortgage interest rates have plunged to record lows, which motivated homeowners to refinance their mortgages, triggering a torrent of principal payments that are passed through to the holders, including the Fed, thereby reducing its balance of MBS. Just to keep that balance level, the Fed would have to buy large amounts of MBS.

过手本金的支付。在作为按揭质押债券标的物的按揭质押贷款得到按期本息偿还或最终偿付完毕的时候,按揭质押债券的持有者会收到过手本金的支付。按揭质押债券的利率已跌至创纪录的低位,房屋的业主借机对原有的按揭贷款进行再融资,提前还贷导致包括联储在内的按揭质押债券的持有者收到的过手本金金额大增,按揭质押债券的未偿余额因此减少。为了维持按揭质押债券的持仓水平,联储不得不大笔买进按揭质押债券。

MBS trades take months to settle. The Fed says they usually settle within 180 days. But most of the time, they settle in 1-3 months. And the Fed books MBS trades after they settle.

按揭质押债券的到期偿还需要数月时间才能清算完毕。联储的说法是整个清算过程通常会在180天内完成,但大多数情况下只需要1-3个月,清算完成后联储才会在账务上体现出来。

So what we see on the balance sheet are not this week’s purchases, but a mix of pass-through principal payments and MBS purchases from weeks or months ago that settled this week. Hence the erratic chart. This week, MBS have remained flat at $1.91 trillion:

因此,当前在联储资产负债表上看到的并不是上周买入按揭质押债券的情况,而是夹杂了过去数周乃至数月买入按揭质押债券以及在此期间受到过手资金并在上周清算完毕的情况,因此下图看上去有点起伏不定,上周按揭质押债券的持仓额仍稳定在1.91万亿美元。

That $248-billion drop in assets in four weeks is a pretty good chunk, even for the Fed’s gigantic balance sheet that was $7.17 trillion four weeks ago.

即使对于四周之前美联储7.17万亿美元的庞大资产负债总量来说,四个星期减持掉2480亿美元也不是个小数字。

I lambasted the Fed for this massive bailout in March, April, and May of the riskiest hedge funds and mortgage-REITs, and the biggest asset holders in the world, to protect them from capitalism’s way of cleaning up those kinds of things. I lambasted the Fed for bailing out asset holders and making sure they don’t have any skin in the crisis while America was in turmoil. So I support the Fed’s backing off this craziness. But obviously, the Fed can turn around on a dime. And every week, the balance sheet may offer unexpected twists and turns.

我在三月份、四月份和五月份的时候已经炮轰过联储对高风险的对冲基金和发放按揭质押贷款的房地产信托基金这些全球最大的资产管理机构给与如此大规模的纾困,以避免这些机构按照资本主义的原则落入破产清算的境地。因此,我支持联储推出这些疯狂的纾困计划。但很显然,美联储随时都有可能来个“原地180度的大转身”,联储每周的资产负债表都有可能出现一些意想不到的波折变化。

免责声明:自媒体综合提供的内容均源自自媒体,版权归原作者所有,转载请联系原作者并获许可。文章观点仅代表作者本人,不代表新浪立场。若内容涉及投资建议,仅供参考勿作为投资依据。投资有风险,入市需谨慎。

责任编辑:郭建

黄金投资平台:www.mt4realty.com